Shorter Filing Deadlines and Expanded Disclosure

New Guidance on "Group" Formation and Cash Settled Derivative Securities

On October 10, 2023, the Securities and Exchange Commission adopted amendments to the rules governing beneficial ownership reporting under Sections 13(d) and 13(g) of the Securities Exchange Act of 1934. The adopting release is available here (the "Adopting Release").1 These rules require investors that beneficially own more than 5% of a public company's equity securities to publicly disclose their beneficial ownership and other related information in either a Schedule 13D or Schedule 13G. The SEC's rule changes:

- shorten the deadline for initial Schedule 13D filings from 10 calendar days to five business days, although they now can be filed until 10:00 pm Eastern Time rather than 5:30 p.m.;

- require that Schedule 13D amendments be filed within two business days of a material change rather than the former facts and circumstances approach;

- accelerate the filing deadlines for Schedule 13G beneficial ownership reports and amendments; and

- expressly require the disclosure of certain derivative securities.

The SEC initially proposed amendments to the beneficial ownership reporting rules in its proposing release published in February of 2022 (the "Proposing Release").2 The SEC's proposed changes received extensive comments, and the final rules make a number of changes from what the SEC initially proposed. Importantly, the SEC did not adopt proposed changes to its rules regarding when a "group" acquires beneficial ownership, and did not adopt a proposed rule that would have included certain cash‑settled derivative securities within the definition of what securities are beneficially owned for purposes of Regulation 13D‑G. Instead, the Adopting Release provides additional guidance and commentary on the parameters around what activities do and do not result in the formation of a "group," as well as when cash‑settled derivatives may result in beneficial ownership of the associated reference securities.

The new rules will be effective 90 days after publication in the Federal Register, which is expected to be soon. However, the compliance timing for the revised deadlines for Schedule 13Gs will not be in effect until September of 2024.

As we have discussed previously, the revised Regulation 13D‑G rules are part of the SEC's ongoing comprehensive update to its regulation of the reporting of securities ownership and the use of derivatives and short sales by private investors, including private funds, hedge funds and family offices. On Friday, October 13, 2023, the SEC continued this project by adopting both new Rule 10c‑1A, regarding the reporting of loaned securities, and new Rule 13f‑2, regarding the reporting of short positions and short activity. The Adopting Release also notes that proposed Rule 10B‑1, which would require prompt disclosure of large security‑based swap positions, including credit default swaps and total return swaps, is still pending and may create additional reporting obligations for investors if ultimately adopted.

I. New Guidance on "Group" Status and Swaps and New Derivative 13D Disclosure Instructions

A. New Guidance on "Group" Formation

In a significant change from the Proposing Release, the SEC did not adopt proposed changes to the rules regarding "group" formation. In particular, the SEC did not revise Rule 13d‑5 to remove the reference to agreements addressing group formation, which may mitigate concerns among investors that the proposed changes set forth in the Proposing Release could result in the formation of groups as a result of mere parallel action, without more.

The SEC reiterates in the Adopting Release that the determination of whether investors are acting as a group "does not depend solely on the presence of an express agreement," and that depending on circumstances, "concerted action" by investors may be sufficient. However, the SEC also stated in the Adopting Release that it is not the SEC's view that a group can be formed "without some type of agreement, arrangement, understanding or concerted action" between investors and that "at a minimum, indicia, such as an informal arrangement or coordination in furtherance, of a common purpose to acquire, hold, or dispose of securities of an issuer" is required.

In response to the concerns raised by many commenters that the new rules and guidance may chill shareholder engagement, the SEC provided additional guidance on the application of the current legal standard for when a group is formed to certain common types of shareholder engagement activities.

Practice point: The SEC did not adopt the proposed amendment to Rule 13d‑5 that would have defined "group" to include investors that tip their intention to file a Schedule 13D with the tippees if the tippees acquire securities of the issuer as a result of the tip. However, the SEC did provide guidance emphasizing that a group may arise under these circumstances "to the extent the information was shared by the [investor] with the purpose of causing others to make purchases in the same covered class and the purchases were made as a direct result of the [investor's] information." Investors seeking to communicate with other investors in advance of filing a 13D, or who are approached by other investors who have a pending 13D filing, should be mindful of this guidance regarding group formation, as well as their obligations under Rule 10b‑5 and the anti‑fraud rules.

Investors looking to understand whether certain activities or communications will result in the formation of a group should be aware of the SEC's new guidance, and its views on the interaction between Rule 13d‑5 and the legal standard set forth in Section 13(d)(3) and 13(g)(3) of the Exchange Act. However, the rule itself has not been changed, and the case law and other interpretive guidance analyzing the facts and circumstances as to whether or not a group has been formed remain good law.

B. New Guidance on Swaps

In a further change from the Proposing Release, the SEC did not revise the rules defining "beneficial ownership" to include certain cash‑settled derivatives. Instead, the SEC extended its existing guidance on how security‑based swaps may confer beneficial ownership of the underlying reference securities to other cash‑settled derivative securities set forth in its release from 2011, Beneficial Ownership Reporting Requirements and Security‑Based Swaps (the "Swaps Release").3 As set forth in the Swaps Release and discussed in the Adopting Release, if the derivative, swap or other instrument confers voting or investment power over the reference securities or the right to acquire such power within 60 days (or at any time if the holder of the instrument is not "passive"), or if the instrument is used with the purpose or effect of divesting or preventing the vesting of beneficial ownership as part of a scheme to evade beneficial ownership reporting requirements, the instrument will confer beneficial ownership over the underlying security.

Practice point: While the guidance highlights certain circumstances under which cash‑settled derivatives may confer beneficial ownership, the SEC emphasizes that "cash‑settled swaps and related derivatives do not generally give rise to beneficial ownership as they do not generally provide voting or disposition rights over the reference securities."

C. Derivative Disclosure Obligations

The SEC has also revised the instructions to Schedule 13D to add express disclosure obligations regarding certain derivative securities, codifying some market practice that already provides such disclosure. Item 6 of Schedule 13D requires disclosure of contracts, arrangements, understandings or relationships with respect to securities of the issuer. The SEC has added to Item 6 an express obligation to include a description of "call options, put options, security‑based swaps or any other derivative securities..."

II. Revised Filing Deadlines for Schedule 13D and Schedule 13G Initial Filings and Amendments

The SEC has revised the filing deadlines and amendment obligations set forth in Rule 13d‑1 (a) through (g) and Rule 13d‑2 (a) through (d), shortening the filing deadlines for both Schedule 13Ds and Schedule 13Gs and generally requiring Schedule 13Gs to be amended more frequently. The changes impact Schedule 13D filers, Schedule 13G filers filing as "passive" investors under Rule 13d‑1(c) ("Passive Investors"), institutional investors filing Schedule 13Gs in reliance on Rule 13d‑1(b) ("QIIs") and Schedule 13G filers filing pursuant to Rule 13d‑1(d) ("Exempt Investors").

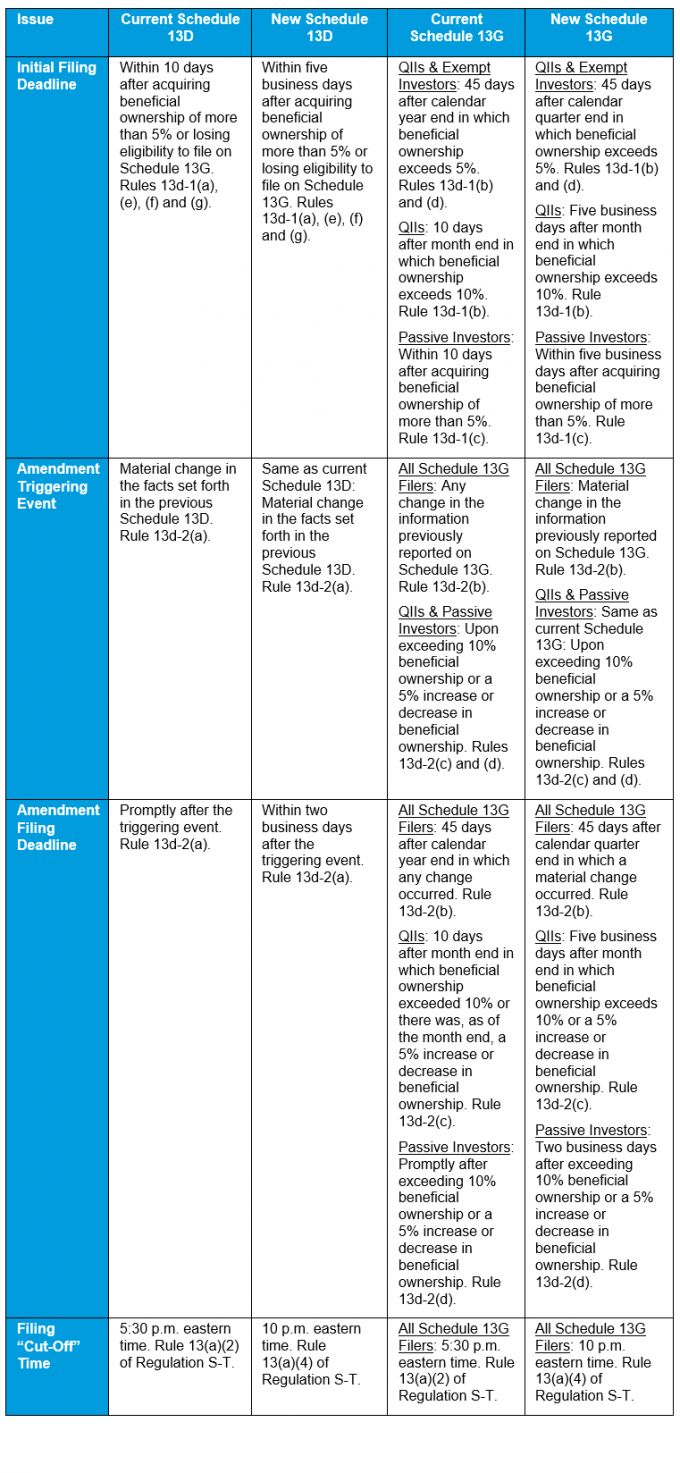

In the Adopting Release, the SEC provided a table setting forth the new filing deadlines as compared to the current filing deadlines, which we have reproduced as Annex A to this Alert.

A. Changes to Schedule 13D Deadlines

Deadlines for Initial Schedule 13Ds

The SEC has revised Rule 13d‑1(a) to require initial filings on Schedule 13D to be filed within five business days, shortening the deadline from the current 10 calendar days.

The SEC made corresponding changes to the rules governing the timing of filing a Schedule 13D after a 13G filer loses eligibility to file on 13G as a Passive Investor or a QII and must transition to a 13D, either because the filer exceeds beneficial ownership of 20% of the issuer securities, is no longer "passive," or no longer qualifies as a QII and does not satisfy the obligations to file as a Passive Investor.4

Deadlines for Amended Schedule 13Ds

The SEC has also amended Rule 13d‑2(a) to provide that amendments to Schedule 13D must be made within two business days of a material change to the information set forth in the Schedule 13D. This is a welcome change for Schedule 13D filers from the SEC's proposal set forth in the Proposing Release, which would have required amendments to be made within one business day of a material change.

The revised rule replaces the prior requirement to file amendments "promptly" after a material change. While courts interpreting what "promptly" meant under the current rules had evaluated the promptness of amendments on a case‑by‑case basis depending on the specific facts and overall materiality of the information being disclosed, typical market practice has been to, in most cases, file amendments to Schedule 13Ds within two business days under the existing rules.

Practice point: Under the revised rules, Schedule 13Ds (and 13Gs) may now be filed up until 10:00 p.m. Eastern Time. However, Current Reports on Form 8‑K filed by public reporting companies are due within four business days and can still only be filed until 5:30 p.m. Eastern Time and get that day's filing date. Accordingly, 13D filers that execute material agreements with a portfolio company may end up disclosing the new agreements earlier than the reporting company, given the accelerated filing deadline for 13D amendments and the ability to file later in the day.

B. Changes to Schedule 13G Deadlines and Timing

QIIs – Initial Filings

Rule 13d‑1(b) permits registered investment advisors, investment companies and other specified entities to file on Schedule 13G instead of Schedule 13D so long as they are "passive" and have acquired the securities in the ordinary course of their business. Under the new rules, QIIs that have acquired beneficial ownership of more than 5% and up to 10% of a company's equity securities will now be required to file their initial Schedule 13G within 45 days of the end of the fiscal quarter in which the QII's beneficial ownership exceeded 5%. This will significantly accelerate the timing of these initial filings, which under the current rules were not required to be filed until 45 days after the end of the calendar year in which a QII's beneficial ownership exceeded 5%.

QIIs that acquire beneficial ownership of more than 10% will now be required to file their initial Schedule 13G, or amend their previously filed Schedule 13G, within five business days of the end of the month in which the 10% threshold was crossed. Under the prior rules, QIIs were required to make these filings within 10 calendar days of the end of the month.

Practice point: If a QII acquires beneficial ownership of more than 5% of an issuer's equity during a quarter, but the QII's beneficial ownership declines to 5% or below as of the end of the calendar quarter, the QII will not have a Schedule 13G filing obligation (unless its beneficial ownership goes back above 5% later). Similarly, a QII that acquires beneficial ownership of more than 10% but whose beneficial ownership declines below 10% prior to the end of the month will not be subject to the accelerated obligation to file within five business days of the end of the month (unless its beneficial ownership goes back above 10% later).

Passive Investors – Initial Filings

Rule 13d‑1(c) permits investors that do not have a control intent with respect to the issuer to file on a Schedule 13G instead of a Schedule 13D, so long as they do not beneficially own more than 20% of the company's securities. The SEC revised Rule 13d‑1(c) to require an initial Schedule 13G filed under this rule to be filed within five business days, rather than the prior 10 calendar days, consistent with the changes to the filing deadlines for new Schedule 13Ds.

Practice point: The SEC has recently taken the position that if an investor that is otherwise eligible to file a Schedule 13G in reliance on Rule 13d‑1(c) fails to file its Schedule 13G within the timeframe specified in Rule 13d‑1(c), the investor loses the ability to rely on Rule 13d‑1(c) and must file a Schedule 13D instead.5 If the SEC applies this interpretation of the rule after giving effect to the amendments implemented in the Adopting Release, the shortened filing timeframe will put additional pressure on Passive Investors to quickly file their initial Schedule 13Gs and avoid the risk of being forced to file on the longer form Schedule 13D, which in some cases can be significantly more burdensome.

Exempt Investors – Initial Filings

Beneficial owners of more than 5% of a company's equity securities that do not acquire securities in a transaction that triggers an obligation to file a Schedule 13D or a Schedule 13G as a Passive Investor or QII must still file a Schedule 13G pursuant to Rule 13d‑1(d). These filing obligations most commonly arise in the IPO context and require pre‑IPO investors that continue to own more than 5% of a company after it goes public to file a Schedule 13G when those investors do not acquire additional shares in the IPO or after the IPO. Previously, these Schedule 13Gs were not due until the end of the calendar year in which the IPO was completed, but will now be required to be filed within 45 days of the end of the quarter in which an IPO is completed, similar to the new timing requirements for initial Schedule 13Gs filed by QIIs.

Schedule 13Gs – Amendment Filing Deadline

The SEC also revised Rule 13d‑2(b), which applies to all Schedule 13G filers, including QIIs, Passive Investors and Exempt Investors, to require amendments within 45 days of the end of each calendar quarter end if there has been a material change to the information reported in the Schedule 13G during the quarter, replacing the current obligation to amend Schedule 13Gs for any change after the end of the calendar year. While the revised rule now has a materiality standard written in, the new quarterly timing requirement may result in significantly more 13G amendments being filed during the year, and will at a minimum require Schedule 13G filers to evaluate their amendment obligations for each Schedule 13G they have filed on a quarterly basis.

Practice point: The SEC declined to add a specific materiality threshold to Rule 13d‑2(b), and Schedule 13G filers will need to evaluate whether a change in information, including changes in their beneficial ownership, is "material" using the standard definition of materiality under the Federal securities laws. While the SEC did say that the 1% ownership change standard for Schedule 13D amendments would be "instructive" for Schedule 13G filers, it is not dispositive.

The SEC also revised the rules applicable to QIIs and Passive Investors regarding when amendments must be filed after the 13G filer's beneficial ownership exceeds 10% of the issuer's securities, and for 5% changes in ownership after exceeding 10% (five business days after month end for QIIs, and two business days for Passive Investors).

Annex A

The following table comparing the new filing deadlines for Schedule 13Ds and Schedule 13Gs to the deadlines under the prior rules was provided by the SEC in the Adopting Release:

Footnotes

1. SEC Release No. 34‑98704 (Oct. 10, 2023).

2. SEC Release No. 34‑94211 (Feb. 10, 2022).

3. SEC Release No. 34‑64628 (June 8, 2011).

4. See revised Rule 13d‑1(e), (f) and (g).

5. See SEC Administrative Proceeding, File No. 3‑21337 (March 9, 2023) at footnote 4.

SEC Strengthens Regulation 13D-G Rules for Beneficial Ownership Reporting

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.