Crowdfunding background

- Comprises Title III of the Jumpstart Our Business Startups Act of 2012, or The JOBS Act (enacted April 5, 2012)

- Originated from two perceived needs:

- that smaller retail investors did not have access to early stage investment opportunities

- that start-up companies did not have adequate access to available capital, particularly online capital raising

- Adds exemption from SEC registration for crowdfunding transactions in the form of new Section 4(6) of the Securities Act

Important SEC Reminder

Information Regarding the Use of the Crowdfunding Exemption in the JOBS Act

On April 5, 2012, the Jumpstart Our Business Startups (JOBS) Act was signed into law. The Act requires the Commission to adopt rules to implement a new exemption that will allow crowdfunding. Until then, we are reminding issuers that any offers or sales of securities purporting to rely on the crowdfunding exemption would be unlawful under the federal securities laws.

- SEC is required to have rules out not later than December 31, 2012

Issuers Not Eligible to Crowdfund

- Non-US companies

- Public reporting companies (only required filers are excluded, not "voluntary filers")

- Investment companies, including companies excluded from the

definition of Investment Company by 3(b) or 3(c) of the Investment

Company Act of 1940, including:

- Mutual Funds

- Private Equity Funds

- Asset Management Vehicles

- Business Development Companies

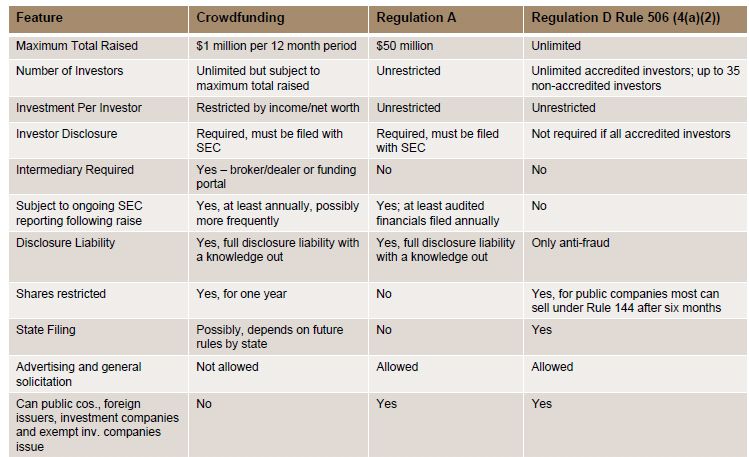

Crowdfunding vs. Other Exemptions

Crowdfunding Requirements

- Raise limits (per trailing 12 month period)

- Company: $1 million

- Investor:

- Less than $100K: greater of $2,000 or 5% of annual income or net worth

- $100K or more: 10% of annual income or net worth

- Must be conducted through broker or "funding portal"

- Must file with the SEC and provide to broker/funding portal and investors extensive disclosure, including tax returns ($100K or less), reviewed financial statements ($100K-$500K) or audited financial statement (>$500K)

Crowdfunding Requirements

- Must not advertise except to direct investors to broker/portal

- Must not pay promoters except as SEC allows

- Must file annual or more frequent reports with the SEC

- Prospectus liability for disclosures with knowledge out

- 1 year holding period on shares sold except to issuer, accredited investor, family member or through registered offering

- Crowdfunded shares do not count towards the 2,000 shareholder rule to force a company public, but see above re SEC reporting

Funding Portals

- Created by Crowdfunding rules

- Must be used as "publicity intermediary" in all crowdfunding transactions

- Exempt from broker-dealer regulation, but must register with FINRA; FINRA can only enforce and examine rules specifically written for funding portals

- Prohibited from:

- Offering investment advice or recommendations

- Soliciting purchases, sales or offers to buy the securities

- Compensating employees based on sales

- Holding, managing or possessing investor funds or Securities

Funding Portal Requirements

- Register with the SEC and any applicable SRO

- Provide disclosures related to risks and other investor

education materials as the SEC shall require

- Must ensure that each investor reviews investor education materials

- Obtain investor representation that he or she understands:

- that entire investment is at risk

- that investing in start-ups and emerging companies is risky

- that crowdfunding investments are illiquid

- Must obtain background check on officers, directors and 20% or greater shareholders

- File with SEC and distribute disclosure materials at lest 21 days prior to first sale date

- Ensure offering proceeds are only provided to issuer when raise has met target; allow investors to cancel orders

- Make efforts to ensure no investor exceeds individual crowdfunding cap across all Transactions

- Protect investor privacy

- Not compensate promoters, finders or lead generators who direct investors to the portal

- Not work with issuers where a portal officer, director or partner has a financial interest

Relationship with State Law

- Crowdfunding transactions are preempted from state regulation

under the National Securities Markets Improvement Act (NSMIA)

- No filing fees may be collected by states

- States may require a notice filing for the state of the issuer's principal place of business or from where 50% or more of the aggregate amount of issue are residents

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.