This is the fourth issue in a planned series of alerts designed to provide an in-depth analysis on topics related to tax reform. This Tax Reform Management Alert issue focuses on executive compensation and employee benefits aspects of the tax reform proposals and how they will impact your business.

On Wednesday, December 20, 2017, Congress passed The Tax Cuts and Jobs Act (Bill). The Senate passed the Bill by a 51 to 48 vote along party lines at about 1 a.m. Wednesday. The House passed the Bill by a vote of 224 to 201 later in the day on Wednesday. (The House had to re-vote due to a technical snafu with their first vote.)

What Happens Next?

President Trump is expected to sign the Bill although, as of the time and date of this Alert, his schedule for doing so is unclear. While the Bill will almost certainly become law and will dramatically reshape the business and individual tax landscape in the United States, the vast majority of the individual tax changes expire in 10 years; however, the corporate rate reduction is permanent. As noted above, the Bill was passed along party lines and, as a result, expect to see efforts to change the law as soon as politics permit it.

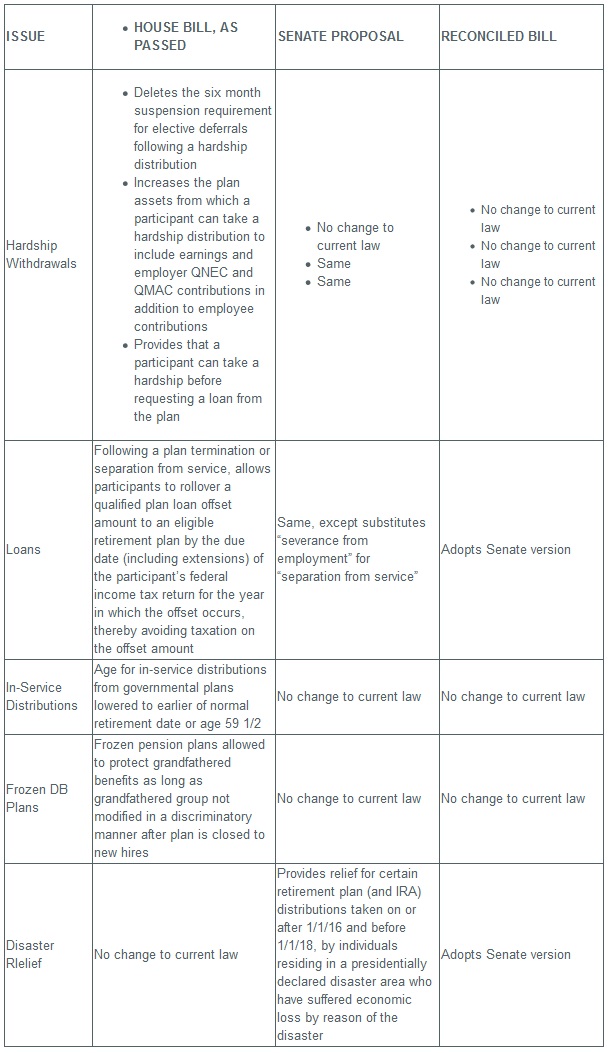

As we've previously reported, the Bill's impact on employee benefits and executive compensation were greatly diminished as the Bill wound its way through Congress (see our previous alerts, Issue #1, Issue #2 and Issue #3). Nonetheless, the Bill does make some important and material changes in this area. The following table updates our prior summaries by providing the highlights of the final Bill, as compared to the earlier versions of the House Bill and Senate Bill.

Executive Compensation

Welfare

Retirement

Seyfarth Shaw will continue to monitor Congressional and regulatory efforts and will alert clients as new developments occur.

Footnotes

1. Generally, an excluded employee is (1) the CEO, CFO (or individual acting in either capacity), (2) family member of CEO or CFO, (3) an employee who has been one of the four highest compensated officers for the corporation for any of the 10 preceding taxable years, or (4) a 1% owner of the corporation at any time during the 10 preceding taxable years.

2. If deferred, the deferred income is taxed upon the earliest of (1) the first date the qualified stock becomes transferable, including to the employer, (2) the date the employee first becomes an excluded employee, (3) the date the stock becomes readily tradeable on an established securities market, (4) the date five years after the first date the employee's right to the stock becomes transferable or is not subject to a substantial risk of forfeiture, whichever is earlier (the Senate version simply provides the date that is five years after the first date the right to the stock becomes substantially vested), or (5) the date the employee revokes the deferral election.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.