In part two of our series on Reductions in Force in Asia Pacific, we addressed the importance of restructuring rationale, employee selection and redeployment, and consultation with employees or employee representatives. In part three, we'll cover the next three issues we recommend multinational employers consider: (#5) severance costs and benefits, (#6) timing challenges, and (#7) logistics and practicalities of implementation.

#5 – Severance Costs/Benefits

As we mentioned in part one of our series, costs and budgeting concerns can affect the overall approach to the RIF.

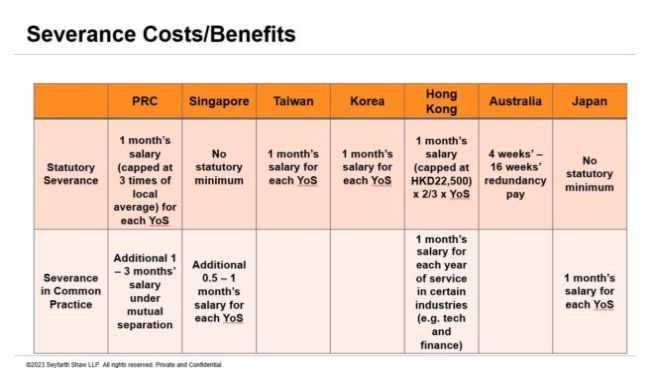

Figure 1: Severance across key APAC jurisdictions

Figure 1 highlights some formulas for statutory severance across popular APAC jurisdictions. We have also included common enhanced severance package benefits.

Other costs/benefits typically include:

- Notice period or payment in lieu of notice (other than in the case of employee misconduct).

- Bonuses, incentive pay, and equity based compensation (usually subject to contractual arrangements).

- In some cases, outplacement services.

This does not take under consideration other costs that may be incurred by threatened or actual litigation or PR issues (e.g., use of HR/business time/resources, legal fees, and/or potential PR/consultancy firm fees).

#6 – Timing Challenges

When planning a RIF in Asia Pacific countries, it's important to consider appropriate timing for employee and public facing communications, including global announcements of any plans to conduct RIFs and, equally, commitments to any timeline for finishing these exercises in the context of the following:

- The target date may not be fixed. Country specific limitations can cause the RIF completion date (i.e., the termination date for all impacted employees) to slip, impacting other operational scheduling issues. Thus, it's important for employers to ensure they don't make any definitive statements too early, especially concerning timing. Announcing unrealistic timing can have an impact on financial results, reporting and RIF costs allocation, as well as employee morale.

- Consultation requirements. Consultations may need to be at least initiated and sometimes completed before potential impacts may be announced.

- Third party employer involvement. Third party employer involvement may mean delays in implementation – sometimes significant ones – created by the time needed for the company notify the Professional Employer Organization (PEO), which may then need to coordinate with their local service provider or employer. Any services contract with a PEO or Employer of Record (EOR) should be consulted for the advance notice required, but even this timeline may slip if there are any disagreements as to the legal requirements and how to proceed. In practice, such disagreements will need to be resolved since it is the third party employer that will take many of the requisite steps.

- Protected employees. For protected employees, including pregnant and sick employees, it's important to determine how long protection will last and whether additional extensions are possible. It may be necessary to carry protected employees on payroll until their period of protection is over and for some period thereafter.

- Local custom/holidays. Global companies need to look out for local holiday periods (e.g., Lunar New Year, Golden Week) when it would be considered bad form or insensitive to undertake reductions. This can include the period in the run up to the holiday or festival period and can also impact the timing of legal advice required, availability of consultation bodies, employees and their representation, and even government authorities and agencies.

#7 – Logistics and Practical Implementation

For a multinational company, particularly one based in the U.S., the logistics of RIF implementation in the APAC region can pose particular difficulties:

- Delivering the news. Again, timing is a key consideration, including time zone differences and who will be available to deliver the news. Practically speaking, a global RIF may need to be "launched" in Asia, or the region may have to "wake up to" news of a RIF from the day before in the U.S. or elsewhere.

- In person/remote meetings. Also critical is determining whether you can have in person or remote meetings, and whether they will be held as a group or individually. In person meetings are typically best, but for larger rounds and in cases where employees work remotely, there is no HR function, or limited HR function in country, at least some of the meetings may need to remote. Also, scheduling large numbers in multiple countries can be tricky whether remote or in person, and there may be technical and logistical difficulties with remote meetings (e.g., unreliable internet, lack of printing or scanning facilities).

- Appropriate representation/power of attorney. This is one item that should be confirmed early on, so that any decisions and terminations are not compromised by invalid, inappropriate, or unauthorized representation of the company, including in locations where local national HR must be making the employment related decisions and actions (e.g., Indonesia). Powers of attorney may be needed to sign termination documents by available personnel and to sign related corporate documents including share transfers and buybacks. It may be necessary to offer retention packages to the key employees who will remain available to execute RIF actions.

- Collecting signatures. For the company, consider where a chop is required and whether coordination with the PEO/EOR is required. It's important to make sure ahead of time that any third party employer representative required for execution is available on the day. For the impacted employee, consider what they will need to sign (not every termination notice necessarily needs the employee's signature, but mutual separation agreements will inevitably require it – the requirements may be more flexible for mutual agreements). If the employee is signing remotely, is a scan sufficient? Do they need to return the original, and how will any required duplicates get where they need to be? Also, consider if there are witnesses required, recommended, and available.

- Removal/resignation of directorships. Consider whether a replacement must be appointed for any impacted directors and whether there are any nationality or residency requirements. Director/shareholder resolutions may be required in the event of forced removal of directors.

- Collecting company property and equipment. Consider what company property and equipment needs to be collected, the tax impact of any equipment being retained by the employee, and the actual logistics of how this will be collected, inventoried, wiped if necessary, and shipped back to headquarters or repurposed locally.

Stay tuned for Part 4, the last in our series on the 10 things to look out for when doing an APAC RIF. We'll cover numbers 8-10 in our top ten list: Consideration of Expats, Post-Employment Considerations, and Risks.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.